Vanguard Study Shows How Incorporating Personal and Household Data Can Significantly Boost Retirement Income for Australian Retirees

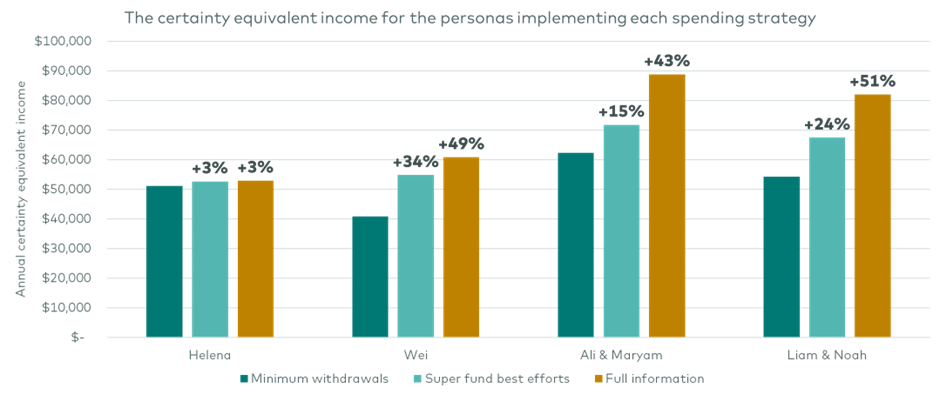

A new study from Vanguard shows that depending on the complexity of their financial circumstances, Australian retirees could increase their projected annual incomes between 3 to 51% by incorporating personal and household data into their retirement income strategies, compared to relying on a minimum withdrawal strategy.

The study findings have implications for retirement advice. While individuals have access to the full scope of their personal information, they may lack the financial expertise to optimise their retirement income according to their financial circumstances. Professional advisers, however, could significantly increase expected retirement outcomes using a greater extent of additional personal information, given their retirement planning expertise. Superannuation funds can also play a role, particularly for members who cannot or do not want to engage a financial adviser, but they are currently limited in their ability to access and use personal information at scale.

The study, which aimed to quantify the financial impacts of greater use of personal information on retirement outcomes, modelled three retirement income strategies that incorporated different levels of personal and household data:

- Minimum withdrawal strategy: Regardless of their personal financial circumstance, a retiree withdraws only the legislated minimum drawdowns from their retirement income account.

- Superfund best efforts strategy: Guidance from a hypothetical superannuation fund that has limited visibility of a member’s financial picture and does not accurately factor in information such as partner status, age pension eligibility, or assets held outside superannuation.

- Full information strategy: An optimised strategy that incorporates comprehensive individual and household information.

The study found that the more personal and household data that goes into a retirement income strategy, the better the outcomes, highlighting the financial benefits of considering personal information in retirement income planning. The study shows that that as a person’s financial situation increases in complexity, so too does the potential value a full information strategy bring.

- As the complexity in financial situations increased, the full information strategy increased projected annual retirement incomes by 3 to 51% compared to the minimum withdrawal strategy.

- As the complexity in financial situations increased, the superfunds best efforts strategy increased projected annual retirement incomes by 3 to 34%, compared to the minimum withdrawal strategy.

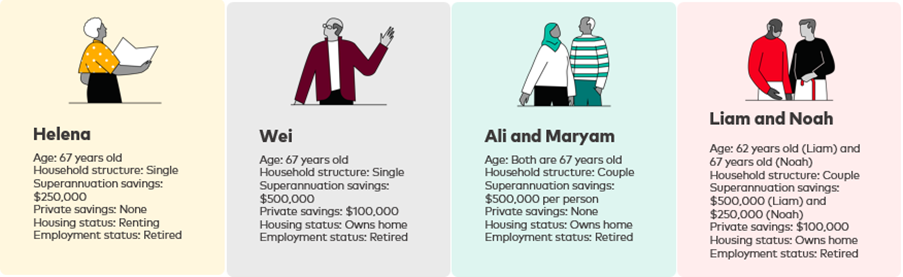

Figure 1 below shows four fictional personas to illustrate the impact of incorporating personal information into retirement income strategies. Superfund best efforts can improve retirement outcomes relative to basic strategies but cannot maximise potential financial value for retirees with complex financial circumstances compared to full information strategies.

Source: Vanguard calculations in AUD as at 1 July 2024 based on VCMM. Percentages rounded to nearest whole number.

Source: Vanguard calculations in AUD as at 1 July 2024 based on VCMM. Percentages rounded to nearest whole number.

Expert Commentary

Vanguard Australia’s Head of Financial Adviser Services Rachel White says the study underscores the importance of personal information in optimising retirement income strategies.

“The study shows that the more personal and household information incorporated into a retirement income strategy, the greater the potential financial benefits. This underscores the critical role personalised financial advice plays in improving retirement outcomes, particularly as financial complexity increases,” said Ms White.

“Comprehensive personalised advice, which combines financial acumen with a person’s full financial picture, is undoubtedly the gold standard. Unfortunately the cost of comprehensive personalised advice and a shortage of advisers make it hard for people to access this level of advice.”

Ms White says given Australia’s growing retirement needs and the potential value advisers can bring to retirement planning, there is a need for settings that encourage a greater supply of advisers in the market.

“Not everyone, however, needs that level of advice, and our research shows that even the consideration of limited personal information and broad assumptions as in the case of the hypothetical superfunds best efforts strategy can already lead to improved outcomes. And that’s a great reminder to make sure you’re engaging with your super fund and making the most of the information and services they provide,” said Ms White.

“With millions of Australians expected to draw down on their super in the coming decade, there’s no time to waste in progressing reforms that uphold consumer protections and enable Australians to safely and easily access personalised advice.”

The information contained in this article is for general information purposes only and does not constitute personal financial advice. You should not act on any of the insights or examples provided without first consulting a qualified financial adviser. This article is sourced from and credited to Vanguard.