The sole purpose of superannuation is to provide members with the financial security to live secure and self-funded lives during retirement.

Yet because we spend years of our working lives attempting to maximise the performance of our contributions — and ensure our money is invested in one of the best performing super funds — many of us fail to give much thought as to how we will manage our super once we retire.

How should you draw on your super when you retire? How long will super need to last for? And how can you best make use of it?

Here are a few things you can do to help manage your super during your retirement years

When can you Access Super?

You can access your superannuation after you meet what the ATO calls a ‘condition of release’.

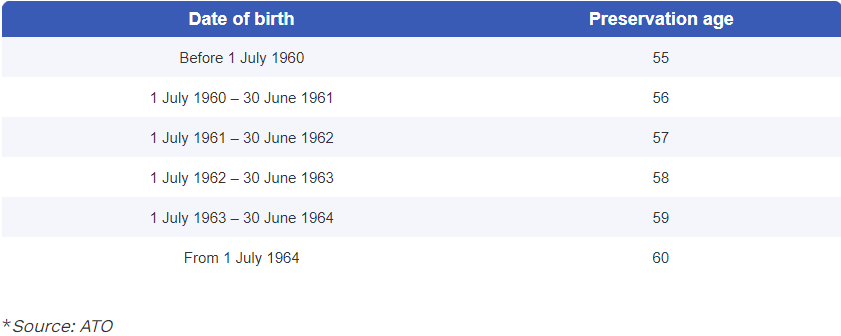

One of the most common conditions of release is reaching your preservation age— the age until which your super must be preserved—and retiring. If you were born after 1 July 1964, your preservation age will be 60 years old, but you may have a younger preservation age, as per the table below, if you were born before then.

Another condition of release is turning 65 years old even if you have not retired. This means you can access your super from this age, even if you are still working.

Retired for the purposes of accessing your superannuation means leaving one job. The ATO says that if you are 60 or over and leave one employment arrangement, but continue in another employment arrangement, you can access all superannuation benefits accumulated up to that time. However, all amounts accrued after that date can’t be cashed out until a fresh condition of release is met.

You can also access your superannuation if you reach your preservation age, are still working and begin a transition to retirement income stream. This kind of pension allows you to transition to retirement by providing access to a small income stream from your superannuation to supplement a wage. It means you can reduce your hours while maintaining the same income.

There are some special circumstances under which you can access superannuation early. The Covid-19 early release of superannuation (ERS) scheme, which allowed people facing hardship to draw on their super, was one of these schemes.

Some of these conditions, for which there are very strict criteria, include severe financial hardship, terminal medical conditions, temporary or permanent incapacity, or a temporary resident departing Australia.

How can I Access Super in Retirement?

There are a number of different ways to access your superannuation once you reach retirement, and retirees or pre-retires, need to think carefully how they do this so they can plan ahead.

Super as a Lump Sum

You can withdraw all of your superannuation in one lump sum, tax-free, once you meet one of the conditions of release outlined above.

As attractive as it may sound to take all your superannuation funds at once, particularly if you have a mortgage to pay off, don’t forget you may have another 20 years for which you may need an income. The aged pension does provide a backup, but you will not be eligible for this until you reach 67 years old if you were born after 1957 and 66.5 years old if you were born between July 1955 and December 1956.

Super as an Income Stream

- The alternative to receiving your superannuation as a lump sum is drawing on it as an income stream or pension. There are a number of different kinds of income streams, the most common of which is an account-based pension.

- Most superannuation funds offer these for members and it is usually as simple as filling out a form specifying how much of your superannuation fund you want to transfer to ‘pension phase account’, what percentage of your balance you want to receive as income and how often.

- There is a minimum annual amount of money which you need to withdraw based on your age and, just like you did before you retired (accumulation stage), you can choose the investment option that suits you best, be it balanced or conservative.

- However, because income on funds in the pension stage are tax free, there is a maximum amount which you can transfer. This measure was introduced to ensure that wealthy retirees did not park too much money in superannuation tax-free.

- This maximum amount a retiree can transfer is called the transfer balance cap and is currently $1.7 million.

- The income you receive from an account-based pension will depend on the size of your funds and their investment earnings. An income stream that provides a guaranteed income for a specified number of years is called an annuity. A deferred lifetime annuity is an annuity that starts at an age that you nominate and will pay a guaranteed income until you die.

- A number of superannuation funds are looking at providing some kind of annuity-type product, but you can also purchase them outside of superannuation. They are attractive to people who are concerned about outliving their superannuation and do not want to live on the aged pension, which currently sits at a maximum of $987.60 a fortnight for singles.

Mixture of Income Stream and Lump Sum in Retirement

You can also take a mixture of a lump sum and a pension in retirement.

Upon retirement you just need to specify to your fund how much you will be taking in a lump sum and how much you will be transferring to a pension account.

Can I get the Age Pension as well as Super?

- If you meet certain asset and income eligibility criteria you may still get some age pension in addition to your super in retirement. In fact, many retirees rely on a portion of the government’s age pension to supplement their superannuation.

- This, of course, depends on how much money and assets (which includes super) you have. If you have too much, you will not be eligible for any of the government pension. The government conducts what is known as an ‘assets test’ and an ‘income test’ to determine if a person or couple qualifies to receive a full, part, or no pension at all.

- A single person can earn up to $190 a fortnight as an income stream and still receive the full pension. Once a single person earns more than $190 per fortnight in Australia the government’s age pension will reduce by 50 cents for each dollar over $190.

- When it comes to the assets test, for a single person, who owns their home, receiving the full pension, the pension will start to reduce when their assets are worth more than $280,000 and $504,500 for someone who doesn’t own a home and is renting.

Remember that even if you have too many assets when you retire to be eligible for the pension, remember that as you draw down on your superannuation (which is considered an asset), you will most likely become eligible for the age pension as your balance decreases.